Many countries around the world are beginning to ease up on blockchain and cryptocurrency, considering that they have proven useful in the midst of the COVID-19 pandemic. Influential figures around the world such as billionaire investor Paul Tudor Jones have also expressed support for Bitcoin, calling it as the best possible hedge against inflation. Crypto regulatory support is known in countries such […]

XPOS in Nigeria. Produced by Multi-jakes

Many countries around the world are beginning to ease up on blockchain and cryptocurrency, considering that they have proven useful in the midst of the COVID-19 pandemic. Influential figures around the world such as billionaire investor Paul Tudor Jones have also expressed support for Bitcoin, calling it as the best possible hedge against inflation.

Crypto regulatory support is known in countries such as Japan, Malta, Switzerland, and Singapore. However, a report by Arcane Research shows that Africa is also becoming one of the most promising places for crypto adoption. Arcane Research discussed that the potential for rapid blockchain and crypto adoption is enormous, and that developments in the continent will likely define the cryptocurrency industry going forward despite overall adoption in the continent being relatively low.

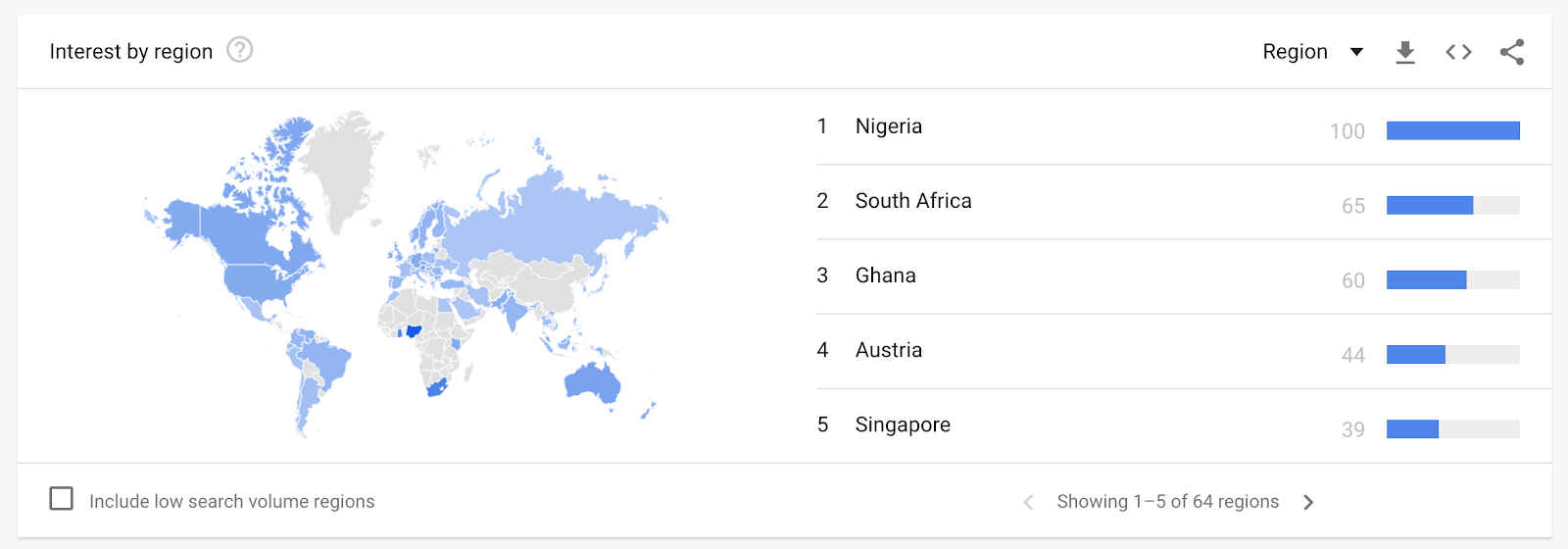

Google Trend data can support this phenomenon as several African states such as Nigeria, South Africa, and Ghana ranked in the top 3 regions that searched about bitcoin, showing that there is growing interest in those countries.

Arcane research also noted in its report that these African nations share a few similarities that led them to exploring the power of blockchain and cryptocurrencies. Some countries are currently experiencing a multitude of economic problems such as high inflation rates, depreciating and volatile national currencies, and capital controls.

Many African states also lack banking infrastructure, as supported by data from the World Bank Group which shows that the number of commercial banks per 100,000 adults in Sub-Saharan Africa is 61% lower than the global average. This disorganization allows Bitcoin and other cryptocurrencies the opportunity to shine and boast their disinflationary and decentralized nature.

Kenya, for instance, has seen a wave of businesses that are accepting Bitcoin as a legitimate means of payment. As of early 2019, Bitcoin transactions in Kenya were valued at over $1.5 million (USD), with many business owners citing the secure nature of the cryptocurrency as a reason for its popularity. Aside from that, it’s also seen as much more convenient than handling paper money.

As a result of cryptocurrency’s growing popularity, the once wary Kenyan government has even formed a task force to look into the benefits of both blockchain technology and cryptocurrency. Developments like these give hope that mainstream acceptance of Bitcoin and other similar assets in the continent will come sooner rather than later.

Apart from Bitcoin and other cryptocurrencies, blockchain technology has been one of the contributing factors to Africa’s digital transformation in the past few years, along with the internet of things, artificial intelligence, and big data. However helpful these technologies are in speeding up Africa’s modernization, the World Economic Forum still recommended governments and educators to primarily educate people in digital and science, technology, engineering, and math (STEM) skills.

Considering that Sub-Saharan Africa has one of the youngest populations in the world, it is now more crucial for governments and other institutions to invest in education to shape the new generation of African workforce with proper skills.

The World Bank also estimated that 1 in 3 people on the planet will live in Africa by 2100, making it more important than ever for the continent to value and enhance its resources and systems.

Fortunately, private companies are making it easier for not just large organizations but simple civilians as well to learn about blockchain and cryptocurrencies. For example, we are helping merchants in Africa accept crypto as a form to exchange for their goods and services through its blockchain-based point-of-sale device, XPOS. The system also allows consumers to acquire cryptocurrency such as Bitcoin, Ethereum or even Pundi X’s native cryptocurrency NPXS on the spot.

With devices such as XPOS being instrumental in the settlement of crypto-based transactions, we can expect more merchants, organizations, and perhaps nations to further accept blockchain and digital currency, integrating them into their daily operations and personal lives.

As we also move forward to the “new normal” because of the impact of COVID-19 pandemic in our economies, digital payments will be more relevant than ever. Data from Statista also shows that the number of mobile proximity payment users worldwide will reach 1.31 billion by 2023, showing that technology will continue to lead major changes in our lives.

We empower blockchain developers and token holders to transact digital assets and services at any physical store in the world. Telegram: http://t.me/pundix